The Paycheck Protection Program (PPP) loans came to save the day for many business owners struggling financially due to the COVID-19 pandemic. However, despite the evident financial relief that these loans came with, very little is understood about the tax implications that PPP loans bring. This article will explain these unique loans, and discuss how they will affect your 2021 taxes.

What Is a PPP Loan?

The Paycheck Protection Program (PPP) is a loan program designed to help small businesses maintain operations after experiencing a financial disruption. The PPP loan is interest-free and provides businesses with up to $100,000 to cover employee salaries and benefits. To be eligible for this loan, businesses must have employees who are not owners or members of the business and must demonstrate that they have been impacted by COVID-19.

Congress introduced this program through the Coronavirus Aid, Relief, and Economic Security (CARES) Act, which aimed at reducing the rate of income loss for Americans. CARES installed the Paycheck Protection Program through the Small Business Administration agency. This enabled small businesses to get loans to help them make paycheck payments and cover other listed expenses. With about $800 billion issued, PPP loans have proven to be a popular recovery plan for many businesses.

Although the PPP is no longer accepting applications (the program ended on May 31, 2021), borrowers may still need to check whether they are eligible for forgiveness of their loans. There may also be tax impacts from their loan.

Are Forgiven PPP Loans Taxable?

No business owner is happy to pay taxes on a loan when their business is barely staying afloat. This explains the growing concern about whether PPP loans are subject to taxation or not.

The CARES Act, which gave provisions for PPP loans, states in section 1106(i) that PPP loans are insured at the Federal level. This means that the PPP loan is exempted from federal income tax charges. However, business owners must first apply for and get loan forgiveness within the first 8 to 24 weeks of receiving the loan to get this exemption.

PPP loans may be subject to taxation at the State level, depending on a business’s state. These kinds of loans are tied to the Internal Revenue Code (IRC), a comprehensive list of tax laws. Certain states have tax laws that conform to the IRC, while others do not. If a business is in a state whose tax laws align with the IRC, the PPP loan will not be taxed even at the state level, provided loan forgiveness was granted.

However, if a business is within non-IRC States, the loan automatically becomes taxable with or without loan forgiveness. Many non-IRC States are trying to find a way to reduce this tax burden for their business owners, but it might take a while for practical solutions to be implemented.

Which Business Expenses Can I Deduct From My PPP Loan?

PPP loans were initially meant to only cover payroll costs. The IRS originally stated that no additional expenses should be deducted, even for forgiven loans. However, this was overturned by Congress in 2020, which means that for the 2021 loans, at least 60% of the amount received is needed to settle paychecks, with the remaining 40% covering operational costs. To be more specific, here’s a brief list of deductible expenses that your loan can cover:

- Wages and gross income

- Gross commissions

- Costs related to employee benefits, such as retirement contributions

- Bonuses and tips

- Paid leave

- Allowances owed for separation or dismissal

- Utilities that were in place before February 15, 2020

- Supplier costs incurred before you applied for the loan

- Operational expenses, like software subscriptions

- Property damage that insurers don’t cover

- Interests for mortgages and car loans, for building and vehicles used in running the business

The CARES Act also clarifies certain expenses that cannot be paid for using a PPP loan. Such expenses include:

- Compensation for employees earning more than $100,000

- Compensation for employees living outside the USA

- Payment of business owners, unless the business is a sole proprietorship

- Payment of taxes

- Payment of fringe benefits like commuter benefits

How to Get Forgiveness for a PPP Loan

Although receiving tax exemption for your PPP loan isn’t guaranteed, getting loan forgiveness is very important. Getting 100% loan forgiveness means you will not have to pay any of the principal amount you received or the interest that would come with it. However, with the PPP loan, any amount that is not forgiven is treated like a two-year loan with a fixed interest rate of 1%. Here’s a simple guide on how to apply for loan forgiveness to get these benefits.

What You Need to Apply for PPP Loan Forgiveness

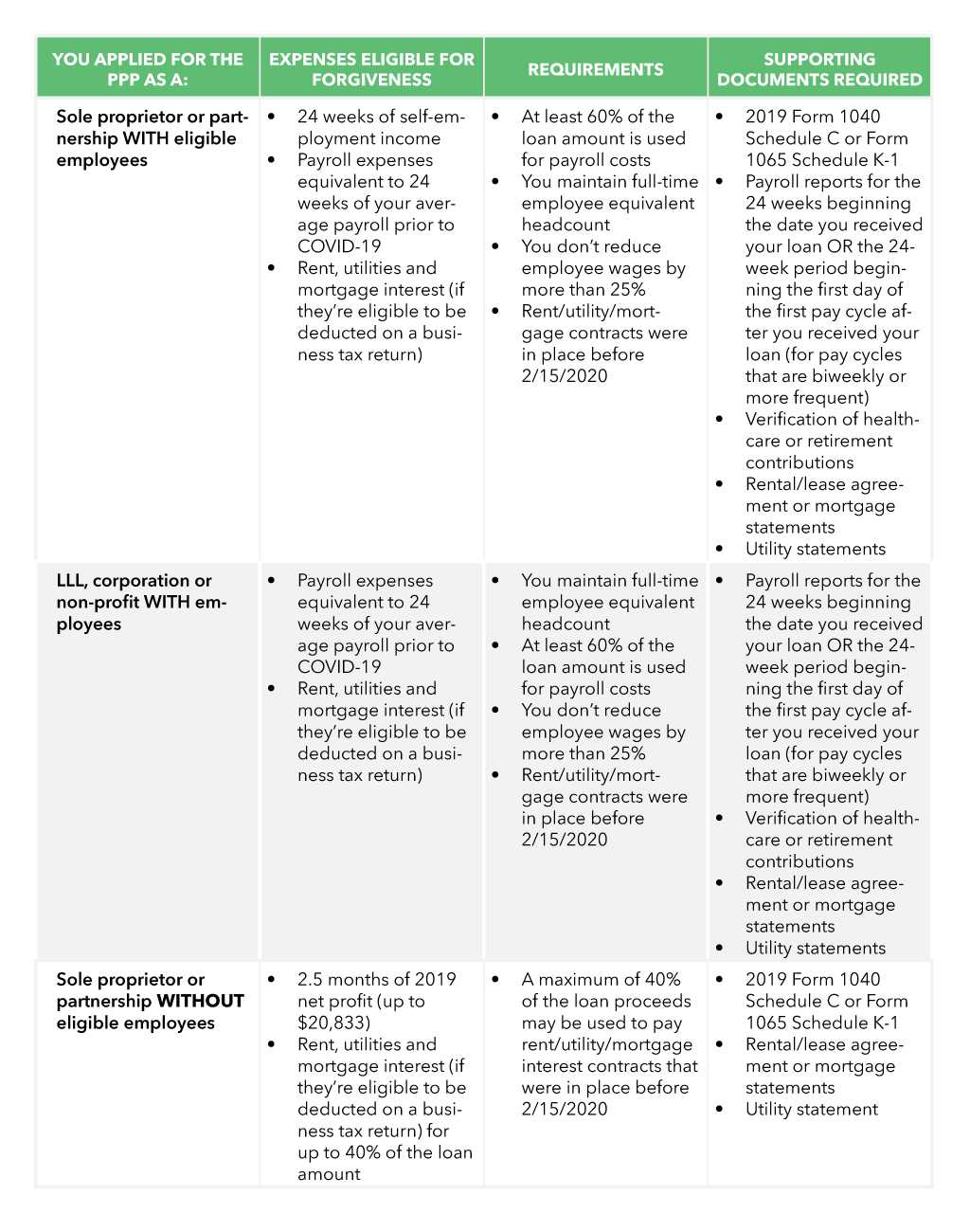

As long as you applied for the loan as a sole proprietorship or partnership business, with or without employees, or as a corporation or LLC with employees, you qualify for loan forgiveness. There are, however, several requirements you need to meet before you get forgiveness for your PPP loan. You must:

- Have used at least 60% of the amount received from the loan to pay payroll costs.

- Have maintained the number of full-time employees you had when applying for the loan.

- Not have reduced employee wages by more than 25%.

- Have had the payment agreements for utilities, rent, and mortgage payments made using the PPP loan in place on or before February 15, 2020.

To back all these requirements up, you will need several documents. Some of the documents you will need include:

- Form 1065 Schedule K-1 or Form 1040 schedule C for sole proprietorship and partnership businesses

- Payroll reports for 24 weeks starting from the first date when you received the loan

- Utility payment statements

- Proof of employee-related contributions

How to Apply for PPP Loan Forgiveness

The application procedure for PPP loan forgiveness is a relatively simple one. Here’s how to apply for PPP loan forgiveness.

- First, fill out the loan forgiveness calculation form.

- Then, fill in the PPP Schedule A Worksheet to prove that you have met the payment requirements and accounted for each employee.

- Finally, fill in the Borrower Demographic Information Form, which asks about your business’s owners, managers, and other relevant stakeholder information.

- Submit the forms and wait for the approval.

PPP Loan Taxation May Differ From State to State

One of the most considerate measures the U.S. government has taken to help small businesses during the COVID-19 pandemic is the PPP loans. These loans have helped keep many businesses operational and employees paid. The loans may have some uncertainty as far as taxation is concerned, especially at the State level. Still, many states are finding ways to exempt them from taxation. It is crucial to check and see what your States’ stance on PPP loan taxation is.

{kind=link}